India’s SME sector powers 30% of the country’s GDP, yet 70% struggle with working capital gaps, per a 2025 IFC report. Traditional banks reject 60% of SME loan applications due to sparse data—leading to ₹15 lakh crore in unmet credit demand. Traditional lending models rely heavily on collateral, credit history, and manual underwriting — excluding thin-file businesses from timely financing.

Working capital lending automation via AI risk scoring changes this: approve SME loans in hours, not weeks, with 95% accuracy. By analyzing alternative data sources such as GST filings, UPI transactions, invoice histories, and cash flow behavior, AI-powered lending platforms help banks and NBFCs approve SME loans faster, reduce defaults, and improve financial inclusion.

This article explains how AI transforms SME working capital lending, key benefits of AI-driven credit scoring, real-world use cases, and how banks can modernize lending operations with intelligent automation.

What is AI Credit Risk Scoring?

AI credit risk scoring uses machine learning and alternative financial data to assess the creditworthiness of borrowers in real time. Unlike traditional credit scoring, AI models analyze GST records, UPI transactions, invoices, bank activity, and behavioral signals to predict default risk more accurately.

How AI Improves SME Lending

- Automates loan underwriting

- Speeds up approvals

- Reduces NPAs

- Improves risk prediction

- Expands lending to thin-file SMEs

- Enables real-time monitoring

The Challenges in Traditional SME Working Capital Lending

A owner of a Pune-based manufacturing firm needs ₹50 lakhs in working capital for a bulk order. His bank demands 3 years of ITRs, bank statements, and collateral. Weeks later, rejection—due to “thin credit file.” He misses the opportunity, stunting growth.

Common pain points in SME working capital financing:

- Data Gaps: 80% SMEs lack formal credit history.

- Manual Reviews: Underwriters spend days on unstructured data.

- Bias and Delays: Subjective scoring misses growth potential.

AI risk scoring flips this with data-driven precision.

Why Traditional Credit Scoring Fails SMEs?

Traditional credit scoring models were designed for large businesses with formal financial histories. However, most SMEs in India operate with limited credit records, informal cash flows, and inconsistent documentation — making them invisible to traditional lenders.

As a result, banks often reject creditworthy SMEs despite strong business potential.

Key Reasons Traditional SME Credit Scoring Fails

- Heavy dependence on collateral and CIBIL scores

- Limited visibility into real-time cash flow

- Manual underwriting delays loan approvals

- Thin-file businesses lack formal credit history

- Static scoring models fail to capture business growth potential

- Human bias impacts lending decisions

For example, a growing SME with strong GST filings and daily UPI transactions may still get rejected because it lacks long-term credit history or collateral.

AI-powered credit scoring solves this gap by analyzing alternative financial and behavioral data in real time.

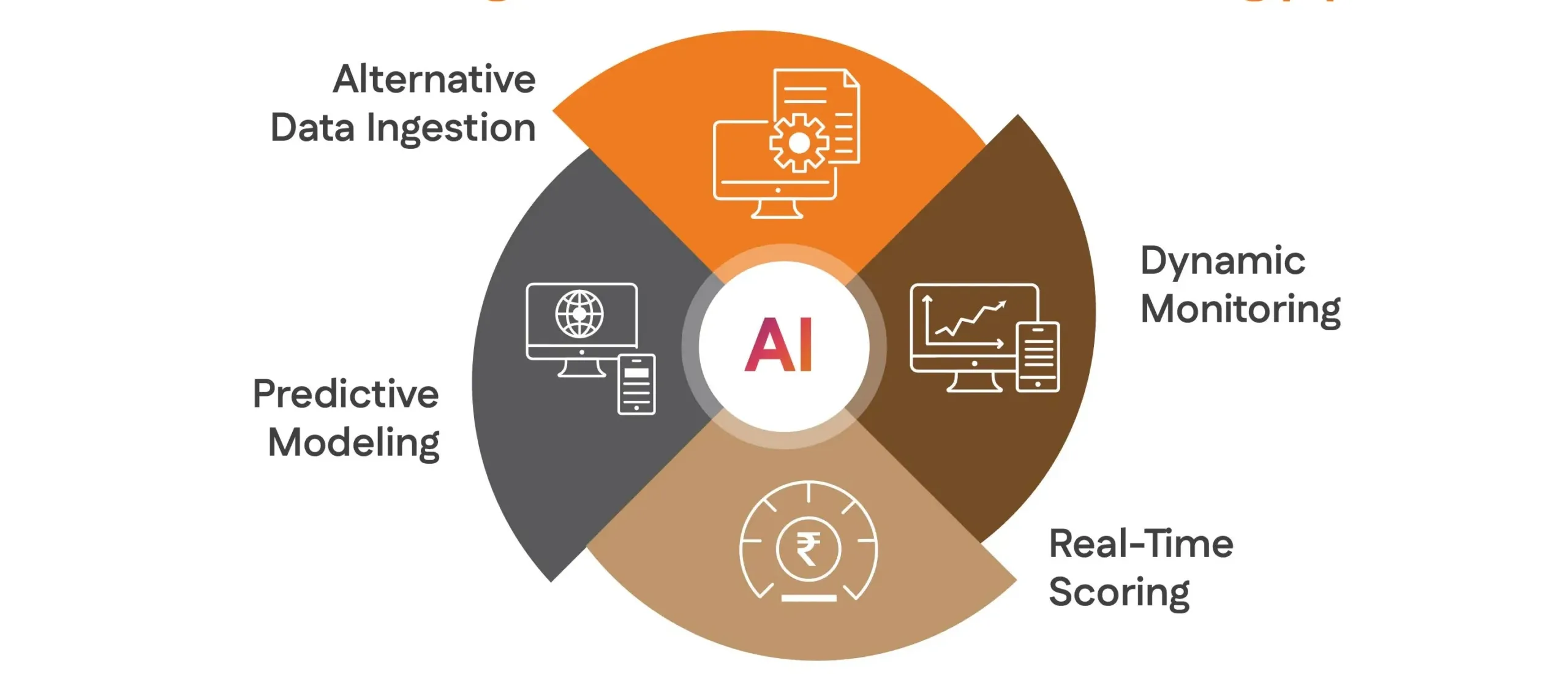

How AI Transforms Working Capital Lending Automation

AI credit scoring for SMEs automates the lending pipeline:

- Alternative Data Ingestion: Analyzes GST returns, UPI transactions, and supplier invoices.

- Predictive Modeling: ML predicts default risk using 100+ variables.

- Real-Time Scoring: Instant scores from 300-850, enabling quick decisions.

- Dynamic Monitoring: Post-disbursal alerts for cash flow dips.

A regional bank automated working capital lending automation. SME borrower ‘s textile firm had no CIBIL score but strong digital footprints. AI scored his 720/850 in 5 minutes, approving ₹30 lakhs—repayment on time, unlocking repeat business.

From Rejection to Rocket Fuel: Anil’s AI Lending Success Story

Anil Sharma, a textile business owner in Surat, needed ₹50 lakhs in working capital to fulfill a large export order worth ₹2 crore. Despite having strong GST records, UPI transactions, and supplier invoices, his loan application was rejected by traditional banks due to a lack of collateral and limited credit history.

He then approached FinqBank, an NBFC using AutomationEdge’s AI-powered risk scoring solution. Instead of relying only on CIBIL scores, the AI platform analyzed alternative data such as GST filings, cash flow patterns, UPI payments, and supplier history.

In under 5 minutes, the AI engine sprang to life. It ingested 100+ alternative data signals, feeding them into predictive ML models—random forests and neural nets trained on millions of SME loans. The system analyzed variables like seasonal sales spikes, supplier reliability (98% on-time deliveries), and behavioral signals (consistent UPI inflows).

With timely funding, Anil completed the order, hired 20 additional workers, and secured repeat business worth ₹3 crore. Over the next six months, his business grew by 40%, while the lender reduced risk and expanded approvals for more thin-file SMEs.

Probability of default? Just 4%.

Loss given default? Minimal.

Score: 745/850.

This shows how AI-driven lending helps banks and NBFCs make faster, smarter, and more inclusive SME lending decisions.

Alternative Data Sources Used in AI Credit Scoring

AI credit risk scoring goes beyond traditional banking records by analyzing alternative data sources that reflect the real financial health of SMEs.

Instead of relying only on balance sheets or credit bureau reports, AI models evaluate digital transaction behavior, operational patterns, and business activity in real time.

| Data Source | How It Helps |

|---|---|

| GST filings | Tracks revenue consistency and tax compliance |

| UPI transactions | Measures daily cash flow patterns |

| Bank statement analysis | Evaluates inflows, outflows, and liquidity |

| Supplier invoices | Verifies business relationships and payment cycles |

| E-commerce sales data | Assesses online business performance |

| Accounting software data | Provides real-time financial visibility |

| Trade and logistics data | Detects business growth trends |

By combining these signals, AI lending platforms create more accurate and inclusive credit risk profiles for SMEs.

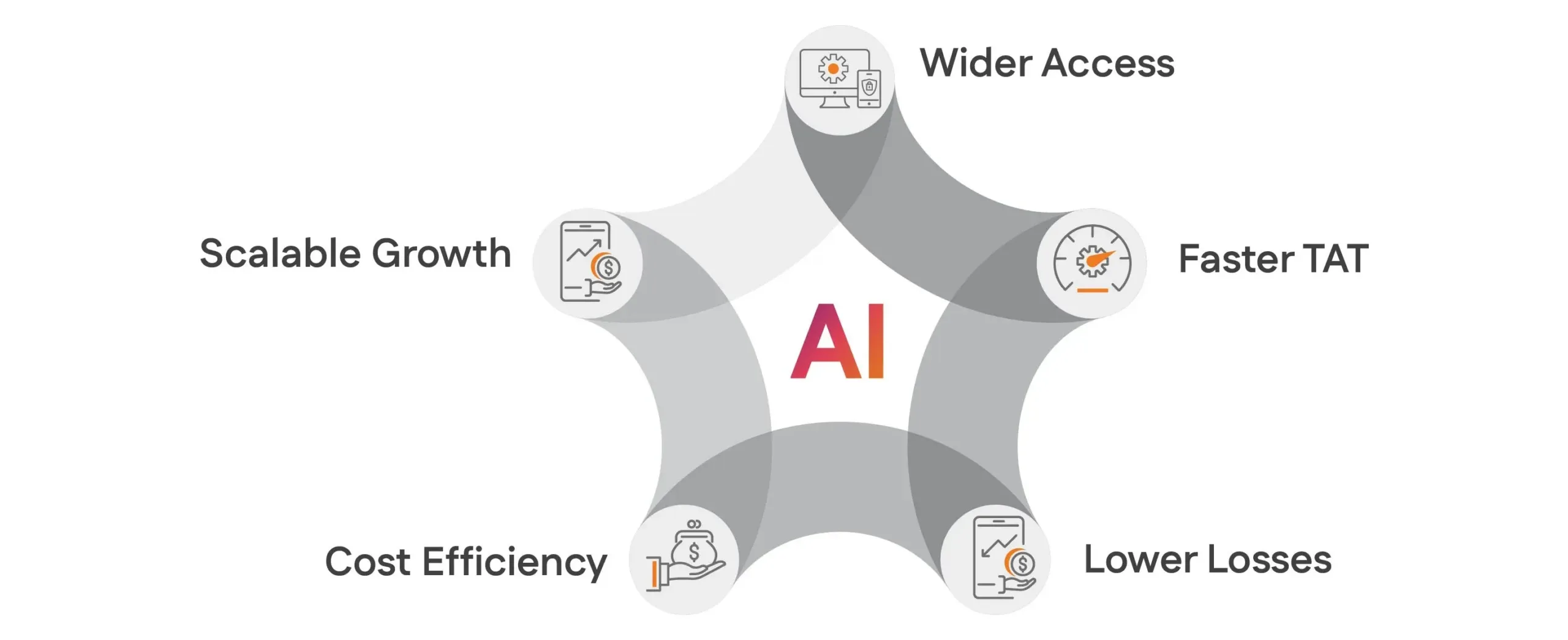

Benefits of AI Risk Scoring for SMEs

AI risk scoring supercharges SME working capital financing:

- Wider Access: Approves 40% more “thin-file” SMEs.

- Faster TAT: From 15 days to 2 hours.

- Lower Losses: Cuts NPAs by 30% via predictive analytics in SME lending.

- Cost Efficiency: 50% drop in underwriting expenses.

- Scalable Growth: Handles 1,000+ applications daily.

| Benefit | Impact |

|---|---|

| Faster approvals | Loan decisions in minutes |

| Lower NPAs | Better risk prediction |

| Wider financial inclusion | More SME approvals |

| Reduced operational costs | Automated underwriting |

| Better scalability | Process thousands of applications |

AI Risk Scoring vs Traditional Credit Scoring

AI risk scoring vs traditional credit scoring reveals stark differences. Traditional methods limit BFSI to formal data, excluding most SMEs. AI unlocks predictive analytics in SME lending for inclusive, accurate decisions.

| Aspect | Traditional Credit Scoring | AI Risk Scoring |

|---|---|---|

| Data Sources | CIBIL, ITRs, bank statements (structured) | 100+ signals: GST, UPI, trade data (alternative) |

| Speed | 7-15 days (manual review) | Instant (real-time ML) |

| Coverage for SMEs | 30-40% eligible (thin files rejected) | 80%+ eligible |

| Accuracy | 70-75% (prone to bias) | 90-95% (predictive models) |

| Adaptability | Static rules | Dynamic learning from new data |

| Cost | High (labor-intensive) | 50% lower (automated) |

| Outcome | Higher rejections, NPAs | More approvals, lower defaults |

This table shows why working capital lending automation demands AI.

RBI and Digital Lending Compliance in India

As digital lending adoption grows, banks and NBFCs must ensure AI-powered lending systems align with RBI guidelines and responsible lending practices.

Modern AI lending platforms support compliance through explainable AI models, audit-ready workflows, consent-based data usage, and transparent credit decisions.

Key Compliance Areas in AI Lending

- Explainable AI for transparent loan decisions

- Consent-driven borrower data collection

- Secure API-based financial data access

- Audit trails for underwriting activities

- Real-time fraud and anomaly detection

- Regulatory reporting automation

- Fair lending practices and bias reduction

AI-powered lending platforms also help financial institutions improve governance while accelerating SME loan approvals.

How Does AI-Enabled Risk Scoring Work?

It builds ML models on historical loan data, alternative sources (GST, bank APIs), and behavioral signals. Algorithms like random forests or neural nets compute probability of default (PD), loss given default (LGD). Output: A score with explainability for regulators. Integrated with core banking, it powers end-to-end AI lending use cases.

How AI Improves Credit Risk Scoring for SMEs

By layering predictive analytics in SME lending on fragmented data. AI detects patterns humans miss—like seasonal cash flows or supplier reliability—delivering nuanced scores. Result: 20% higher precision in working capital lending automation.

How AI is Used in Lending

AI is used in lending spans use cases:

- Origination: Auto-score applications.

- Monitoring: Flag deteriorating risks.

- Collections: Predict recovery odds.

Role of Generative AI and Agentic AI in SME Lending

The next evolution of SME lending is being driven by Generative AI and Agentic AI systems that automate decision-making, customer interactions, and underwriting workflows.

While traditional AI predicts risk, Generative AI helps banks generate insights, summarize financial data, and automate borrower communication. Agentic AI goes a step further by autonomously orchestrating lending workflows with minimal human intervention.

How Generative AI Helps SME Lending

- Summarizes borrower financial profiles instantly

- Generates underwriting recommendations

- Automates loan document analysis

- Assists relationship managers with AI copilots

- Speeds up customer onboarding and KYC workflows

How Agentic AI Transforms Lending Operations

- Automates end-to-end loan orchestration

- Continuously monitors borrower risk signals

- Triggers proactive risk alerts and collections workflows

- Coordinates across LOS, LMS, CRM, and core banking systems

- Enables autonomous lending decisions at scale

Together, these technologies help banks reduce turnaround time, improve underwriting accuracy, and scale SME lending operations efficiently.

AI Credit Scoring for SMEs in Action

A NBFC deployed AI credit scoring for SMEs, processing 200 daily SME working capital financing requests. Predictive analytics in SME lending analyzed trade data, approving 75% instantly. NPAs fell 28%, with ₹500 crore disbursed in Year 1.

Future of AI in SME Lending

AI is rapidly transforming SME lending from a manual, document-heavy process into a real-time, intelligent, and autonomous financing ecosystem.

In the coming years, banks and NBFCs will increasingly adopt AI-driven lending platforms that can predict borrower behavior, personalize loan offerings, and automate credit decisions instantly.

Emerging Trends in AI-Powered SME Lending

- Real-time AI underwriting and approvals

- Embedded finance and API-driven lending

- Autonomous lending workflows with Agentic AI

- Hyper-personalized loan offers

- AI-based fraud prevention and anomaly detection

- Continuous borrower risk monitoring

- Voice and conversational AI for customer onboarding

- Predictive collections and recovery automation

As competition intensifies, AI-powered lending will become essential for scaling SME financing while reducing operational costs and credit risk.

AutomationEdge SME Working Capital Solutions with AI

AutomationEdge delivers SME working capital solutions with AI through our agentic platform. Request an AI credit risk scoring solution demo to see seamless integration with core systems. We’ve empowered banks with working capital lending automation, achieving 98% accuracy and 60% cost savings. Scale your SME portfolio—contact us today.